Photo by Wolfgang Hasselmann on Unsplash

This post is following of above post.

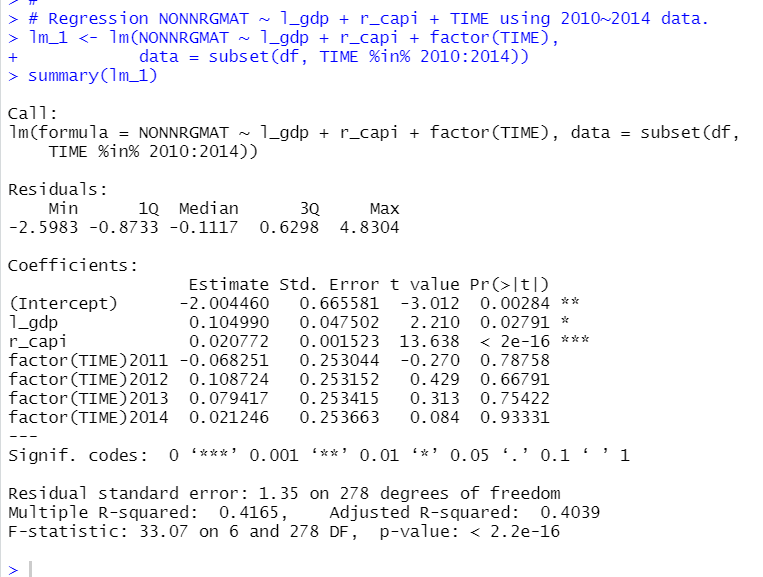

From the previous post, NONNRGMAT has correlated to r_capi: squared rooted per capita gdp. Let's do regression analysys using R.

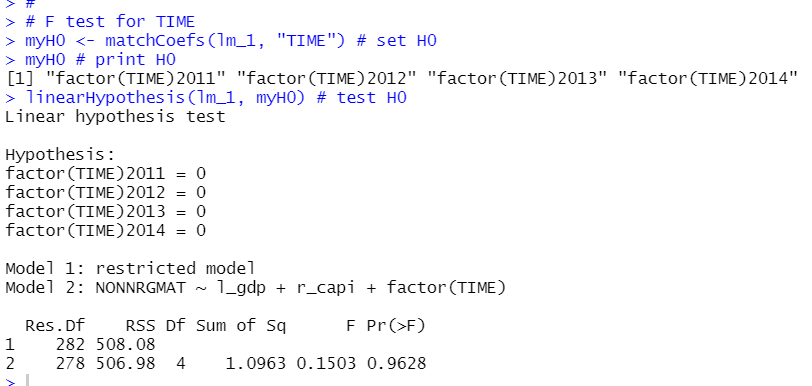

p-value for r_capi is almost 0. For TIME variables are not significant. Let's check if there are jointly significant. I use car::linearHypothesis() function.

I used matchCoef() function to make my Null Hypothesis. Then, I use linearHypothesis() function. The result shows p-value is 0.9628. So, TIME is not jointly significant.

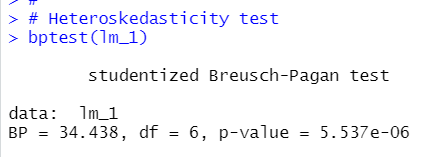

Then, let's check if residuals is Homoskedasticiy or Heteroskedasticiy.

I use bptest() finction in lmtest package.

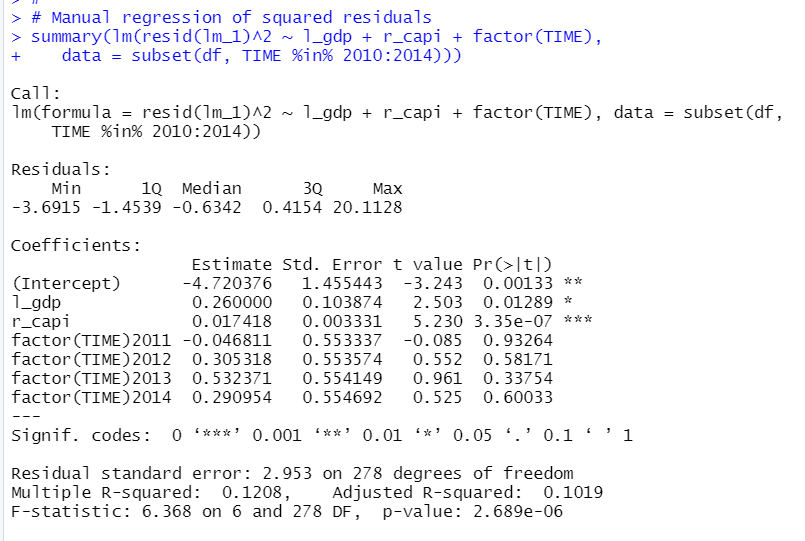

p-value is almost 0. So, this regression model has Heteroskedasticiy. Let's confirm lm() function and resid() function.

p-value is 2.689e-06, it is almost 0. So, we reject Null Hypothesis: residual is Homoskedasticity.

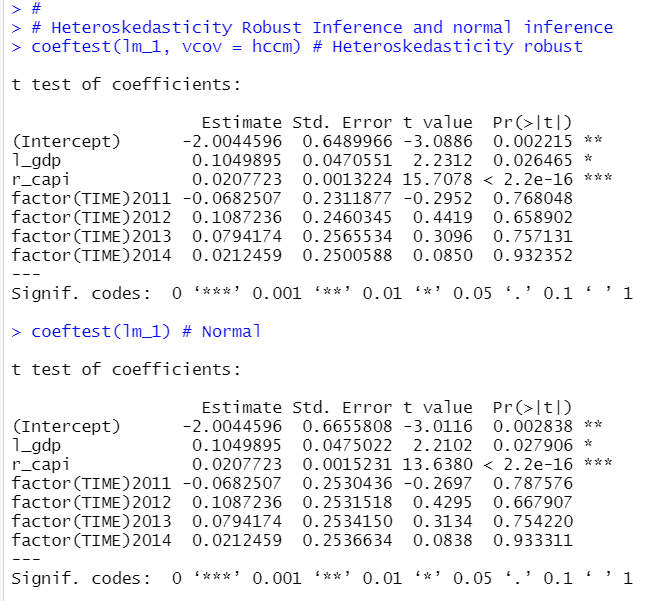

So, I compute Heteroskedasticity robust standard error with lmtest::coeftest( , cvov = hccm) function.

The conclusion does not change. l_gdp is significant at 5% level, r_capi is is significant at 0.11% level or below.

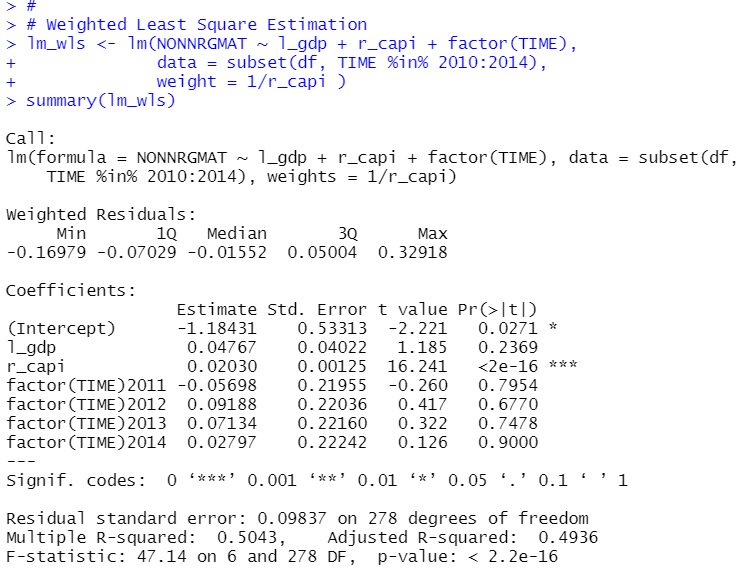

Next, let's do Weighted Least Square estimation. I use "weight = 1/r_capi" in lm() function.

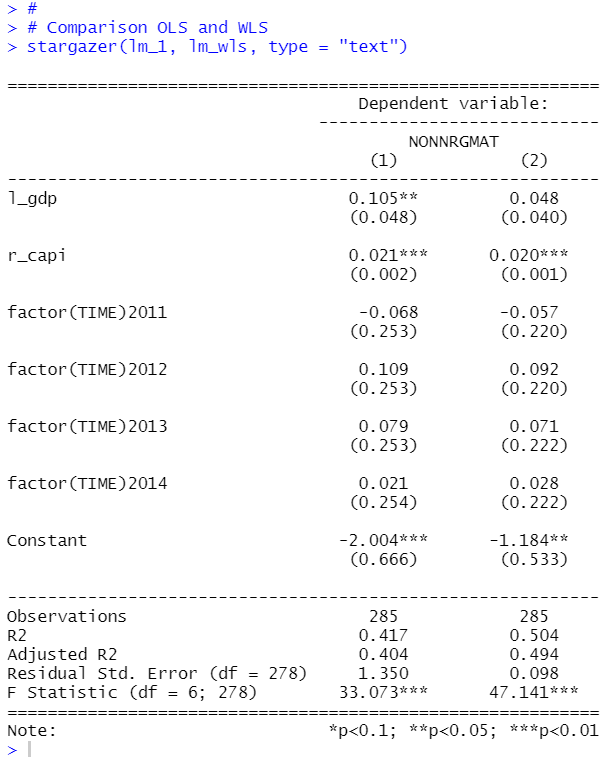

Let's compare OLS estimation(lm_1) and WLS estimation(lm_wls) with statgazer package.

(1) is OLS and (2) is WLS. There is not significant change between OLS and WLS for r_capi coefficient.

That's it. Thank you!

Next post it

To read from the 1st post,